Inside My Alternative Portfolio — Part II: Deal-by-Deal Results (2026 Update)

- Mar 8

- 23 min read

By Ian Ippolito · Last updated May 4, 2026 · Code of Ethics

In Part 1, I explained the strategy, allocations, and overall performance of my alternative portfolio. Here in Part 2, I go deeper into the individual investments — including real estate, GP stakes, litigation finance, music royalties, private equity, search funds and more — along with income, distributions, lessons learned, and future plans. And I also discuss cash management, taxes and what I'm looking at going forward.

(Usual disclaimer: I'm just an investor expressing my personal opinion and am not an attorney, accountant nor your financial advisor. Consult your own financial professionals before making any financial decisions. Code of Ethics: To remove conflicts of interest that are rife on other sites, I/we do not accept ANY money from outside sponsors or platforms for ANYTHING. This includes but is not limited to: no money for postings, nor reviews, nor advertising, nor affiliate leads etc. Nor do I/we negotiate special terms for ourselves in the club above what we negotiate for the benefit of members. Info may contains errors so use at your own risk. See Code of Ethics for more info.) This is Part 2 of my 2026 portfolio update. In Part 1, I covered the overall strategy, allocations, and performance of the portfolio.

Why so much real-estate?

As you saw, 70.9% of my alternatives portfolio is real-estate.

So the first thing many people ask me, is: "Why so much?"

One reason, is that a landmark study found that real estate’s long-term, raw returns have been comparable to the stock market (7 - 8 % real returns...which means "after inflation"):

From the study The Rate of Return of Everything, summarized here

Notes: "equity" is the stock market and "housing" is real-estate. And real-estate returns reported are un-leveraged (i.e. prior to the affect of adding any potential debt).

...but real-estate has done it with less volatility:

From the study The Rate of Return of Everything, summarized here

Note: "equity" is the stock market and "housing" is real-estate.

...and that's not all.

Investors who understand how to use real-estate tax deferral techniques like depreciation and "defer, defer and die" can produce after-tax outcomes that stocks simply can’t match.

As an example, a 7% tax-deferred real-estate real return is equivalent to 9.19% taxable stock market real return (when taxed at long-term federal capital gains rate of 23.8%). This is significantly more than what stocks have actually returned over the long-run. And real-estate's return becomes even higher, if an investor lives in a state with state income tax.

And over time, the compounding difference between taxed and tax-deferral can be dramatic:

In this scenario, two identical series of investments produce $898,000 when taxed and $2.05 million when tax-deferred -- a 128% increase -- simply for deferring tax.

So real estate is one of primary legs that support the stool of my portfolio (along with stocks, non-real-estate alternative investments and U.S. Treasuries).

Last Year's Returns

Okay with that out of the way, let's jump into how each individual investment did.

Important note (March 7, 2026): Year-end valuations are not yet available for most private placements. And these typically arrive in late spring or summer due to the extensive year-end work required for audits and reporting. So normally I would wait for those before publishing this update. But many readers have been asking to see many of the other portions of this deep-dive and are also interested in my thoughts on how AI may affect future investments. So for now, I’ve marked those valuations as TBD (to be determined) and also marked portfolio-level returns the same way. Returns derived solely from income or realized exits are not affected by valuations and are shown below.

Here's a summary:

And here's how these were calculated:

MG Properties income was all tax-deferred. Since all other returns are reported on a pre-tax basis, the tax-deferred return (4.51%) was converted to an equivalent taxable-return (using our marginal federal tax rate of 37% to get 7.16%). We live in Florida and have no state income tax. But if we lived in a state that had one, the equivalent taxable return would have been higher. See MG section for full details.

J-curve: Many alternative investments have an initial investment period (typically in the first few years) during which they are deploying funds and are not yet making full distributions. So I didn't include these in total return calculations at the top (even though you can see that some are producing healthy returns like GP Stakes, Search fund sponsors). So that reduced the % return shown a little lower than it should have been. Once out of the J-curve, they will move up to the top (and be included).

Residential rental real estate pricing: I used Zillow's home pricing tool (the Zestimate) for this. Many investors (including myself) feel Zillow generally underestimates prices. If that's the case here, then the actual price appreciation % return is higher than shown.

% instead of IRR: For simplicity, returns here are shown as percentages (which most people understand) rather than IRR. IRR can be deceptively tricky, even for experienced investors. In addition, IRRs are relatively easy for sponsors to manipulate. And I also feel that an exclusive focus on maximizing IRR can sometimes become a trap that inadvertently encourages riskier behavior that is destructive over the long term. For example, IRRs tend to be higher for short-term “flips” or aggressive deals than for more conservative, long-term buy-and-hold investments.

So I view IRR as one useful tool in the toolbox (along with metrics like MOIC and others) -- but not “the one metric to rule them all” that some investors treat it as.

Investment-by-Investment Deep-Dives

Here's a deep dive look at what's happening on each investment (from the largest to the smallest holdings):

1) Residential rental properties: (same as last time at #1)

This is by far the biggest part of my alternatives portfolio. Again, I follow the core-satellite approach to risk. And this large conservative core lets me feel comfortable taking more risk on smaller satellite portions. Residential renters tend to be more stable and longer term than multifamily/apartment renters, which I like. I target working class neighborhoods with affordable rents (to maximize the renter pool, and align myself with the long-term trend of a growing lack of affordable housing). I also pick neighborhoods that are low in crime (avoiding class-C) and properties that meet my yield and other minimums. These were purchased with no debt, which I believe hardens them extremely well against a severe downturn. The vast majority of real estate investors would probably consider this to be an outrageously conservative strategy that leaves too much money on the table. And they would would prefer higher projected returns by taking on leverage, instead. On the other hand, the strategy works for my purposes. This returned 6.37% (income + price appreciation). And 5% was returned in income alone. In past years, income was higher (6% -7%+). This year, there was some bad luck and unusually high turnover. That resulted in longer than normal periods of time where multiple properties were vacant -- and made turnover expenses much higher than normal. Next year, I expect income to move upwards toward the average. The price appreciated 1.37%, which was a slow-down from last year. In the crazy post-Covid-19 days, it skyrocketed 20-30%+ for multiple years. So this reversion down to the long-term average was expected. I regularly cull this portfolio when a property falls out of my minimum criteria (if the neighborhood looks like it's going bad or if there's too much turnover, etc.). This time there weren't any house sales.

My goal is to deploy additional cash into this asset class. But it will depend on pricing, etc., so we'll see what happens. Also, I'm not willing to buy rentals in a remote city via a turnkey operator, because I feel there are too many financial incentives and ways for operators to hide significant problems that I'd never even realize. So if I can't redeploy here, I'll keep it in cash or find some other place for it.

2) MG Properties Group (versus #2 last time)

Last update, I was diversified in nineteen different properties with this sponsor across multiple funds. Since then, I've added additional money and will end up being in about twenty four or so.

MG Properties is one of those very rare sponsors that has a record spanning multiple cycles without losing any investor money. They do multi-family value-added, using moderate leverage, and high skin in the game (10 to 33%). They also are one of the few to implement a full-featured 1031 exchange pipeline, which allows taxpayers to defer all taxes indefinitely. See this article on: "How to Invest in Passive Real Estate Without Paying a Penny of Tax (Legally): Part 2: "Defer, Defer and Die". This is generally a long-term 7 to 10 year hold. And on exit, I intend to 1031-exchange into a follow-up investment with MG (to defer capital gains tax). Ideally, I would like to hold a position with them forever, and when my wife and I pass away, pass it on to our son (who would inherit it on a stepped-up basis, and also not pay any capital gains). This is all part of the "defer, defer and die" tax minimization strategy mentioned above.

This year, I was happy with the % income generated, which I felt illustrated the dual advantages of vintage year investing strategy and tax deferral. In a year when many aggressive deals imploded, it returned 4.51% tax-deferred. That's equivalent to 7.16% taxable return (at our incremental federal tax bracket of 37%). And Florida doesn't have states taxes. But if I lived in a state with an income tax, then the equivalent taxable return would have been even higher.

As you can see above, a few of my MG investments are still in the J curve (meaning not fully deployed and/or not producing full distributions). So this makes the overall % shown a little lower than it should be (versus if I had properly split out the portions that are deployed .. from those that aren't). But, it was too much work to do that. So for these purposes, I just kept it the current way.

How could such strong performance happen in a down-turn recovery and when so many other real-estate deals have done so badly?

The first key was the diversification that was carefully and patiently implemented over many vintage years. The 2021-2022 vintage years turned out to be down-years (and are underperforming at 2.15% and 0.05% respectively). But the non-downturn-years are much stronger and higher (from 2.95% to 7.75%). So they picked up the slack:

The second key was having the discipline during the long, two-decade up-cycle (2010-2020) to avoid many aggressive deals with flashy, high projected returns in the first place.

This was not always easy. In contrast, MG deals are boring and conservative (with lots of skin in the game, conservative leverage and reasonable waterfalls). The idea is to minimize the chance of large, realized losses in a down-turn. So my MG investments are doing exactly what I'd hoped they'd do—avoiding disastrous defaults and painful distressed sales, so they can benefit when the cycle fully recovers. And in the meantime, they're throwing off nice income and tax benefits.

For the upcoming valuation: In a previous portfolio update, MG adjusted their price values down to reflect the down-turn. Many sponsors didn't do this and I appreciated the transparency.

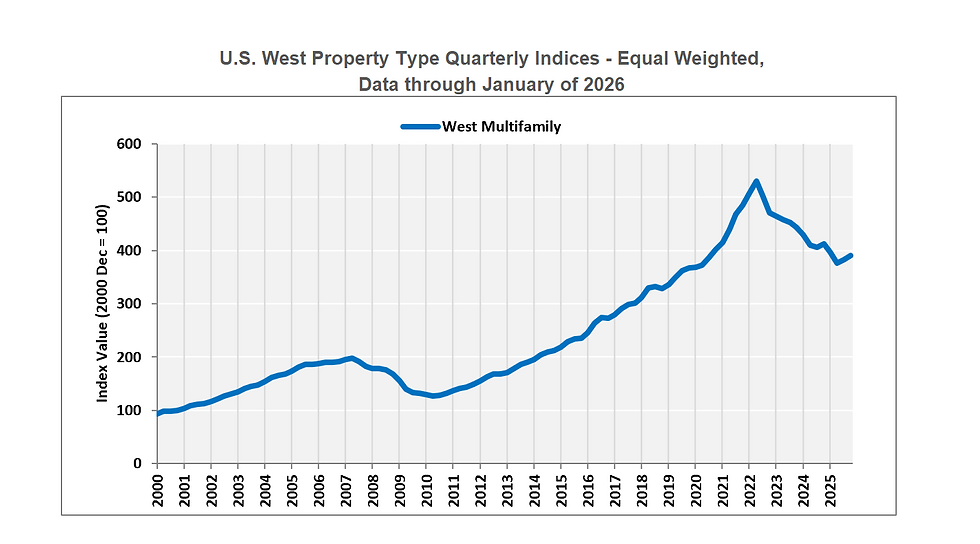

This year, properties in the West had a small bump up (reflecting a generally recovering market):

So I wouldn't be surprised if valuations also show a small bump up, too. At the same time, real-estate performance can be very localized and individual property situations can override wider trends. So we'll see. Either way: Since MG deals aren't distressed, I don't put too much value into interim valuations (which are based on a hypothetical situation that isn't actually happening... a distressed sale in the current down-cycle). The ultimate total return is much more important to me. At the same time, I also fully expect interim valuations to ultimately increase as well (as the cycle continues to move forward).

3) GP Stakes (vs #3 last time)

GP stakes is a niche asset class that's isn't widely known (beyond institutional investors who keep it closely held). The core of its profitability tends to be uncorrelated to economic cycles, stock market, etc. (which can provide helpful diversification to a portfolio and cash flow).

Here's how it works. The GP stakes fund purchases an equity share (stake) in a private equity company (the GP). This entitles it to receive a share of GP management fees, promotes (profit splits), balance sheet income (co-investments) for all current funds (and any new ones that are created). And the cash flow and downside protection from the management fees tend to be extraordinarily stable and predictable (even without growth). Then, the other income factors (promotes, balance sheet income) provide opportunity for extra upside return. Not all GPs are created equal and the top tier tend to be much more reliable and less volatile than the rest. So I don't feel comfortable bottom-fishing in this asset class. And I'm also very picky about which funds I invest in, so I require a team that has a very long track record of experience and success.

I was very happy to find an additional fund to invest in this asset class over the last year (fund II of a sponsor I had already invested in). This brings my total to three. These sponsors have requested their identity to be kept confidential in this article. Club members can get full info including their name, as well as detailed due-diligence, etc. here and here. (Membership is free but requires verifying that the applicant is truly an investor and has no conflicts of interest).

All of these funds are not yet full deployed (and still in the J-curve). However a nice benefit of this asset class, versus some other private equity types, is that it tends to produce some income even then. This year overall income was about 7.4% (with return from price-appreciation TBD). And as they continue to deploy, and the GPs have a chance to raise new funds and earn extra promotes, I expect the total return to increase over time.

4) Traditional Private Equity (unranked last time)

Traditional private equity is one of the largest alternative asset classes globally. PE firms purchase companies, improve their operations and growth prospects, and eventually sell them at a higher valuation.

Historically, top-tier private equity managers have generated strong returns relative to public markets.

Source: Fidelity

But unlike public markets, the dispersion of results between managers is enormous. The best funds can significantly outperform, while mediocre ones often lag public markets. Because of that, manager selection is extremely important in this asset class.

Source: Fidelity

Since the last update, I was very happy to find three funds to invest in this asset class. These sponsors have requested their identity to be kept confidential in this article. Club members can get full info including their name, as well as detailed due-diligence, etc. here (#1 + #2) and here (#3). (Membership is free but requires verifying that the applicant is truly an investor and has no conflicts of interest).

I'll talk about what they do without mentioning any names:

Lower middle-market buyout: This niche-based private equity firm has a long record of multiple-cycle experience (and no fund-level losses) and has consistently delivered top quartile results. The fund targets smaller companies that tend to be less efficiently priced than large public businesses. This can create opportunities for an experienced operator to add value through operational improvements and strategic growth. This is currently in the J-curve (deploying into assets). Distributions aren't expected until the assets mature and are harvested (which generally takes several years).

Small-buyout fund: This is another established private equity sponsor with a long track record of multiple funds, desirable top-quartile performance, no fund-level losses and high skin-in-the-game / co-investment. Smaller buyout strategies are often considered an attractive niche within private equity because they target companies that are too small for the largest PE firms but still have significant growth potential. This segment has historically produced strong returns, although access is typically limited. This is currently in the J-curve (deploying into assets). Distributions aren't expected until the assets mature and are harvested (which generally takes several years).

Cherry-picker: The third investment takes a different approach. Rather than operating as a traditional buyout fund, it co-invests alongside top-tier private equity sponsors in individual deals (diversified by industry, size and vintage year). They also have a very famous political house-hold name as a principal, who gives them fairly unparalleled access to decision-makers and deals around the world. As a result they invest in major PE firms like KKR, Apax, TA Associates and others, while also avoiding the typical additional layer of fees that many co-investment funds charge.

This is currently in the J-curve (deploying into assets). Distributions aren't expected until the assets mature and are harvested (which generally takes several years).

5) Search Fund Sponsors (unranked last time)

Search funds are a little-known niche asset class that's performed very strongly in past recession vintage-year groups.

They focus on buying microcap market companies with strong growth, recurring revenue streams and stable free cashflow generation. So this put them somewhere between the typical venture capital (VC) and private equity (PE) funds. The companies are more established and stable than VC funds, but too small for a typical PE fund.

Historical performance has been strong with 30%+ gross IRR and 5x+ gross ROI (over multiple decades and cycles from 1984). And they've had positive performance in multiple vintage year groups containing a recession.

A search fund sponsor is one who creates a fund that invests in multiple search funds (for added diversity).

I invested in three new search fund sponsors since last time (bringing my total to six). The sponsors have requested that their identity be kept confidential in this article. Club members can get full info including their names, as well as detailed due-diligence, etc. here. (Membership is free but requires verifying that the applicant is truly an investor and has no conflicts of interest). All of these are currently in the J-curve (deploying into assets). Distributions aren't expected until the assets mature and are harvested (which generally takes several years).

Despite that, one of them had a very large, early exit, resulting in a YTD return of income/exit proceeds of 15.25%. This was a pleasant surprise (and not something I expect to happen again next year).

6) Litigation Finance (versus #5 last time)

Litigation finance investments provide financing to law firms that need money to pursue cases with a higher than normal probability of success. It's not directly correlated to the business cycle/recessions, which can be great protection and diversification to a portfolio during a downturn/recession.

The asset class is becoming a favorite for institutional endowments and large family offices, but very difficult for most investors to access. Projected returns can be 18 to 20% IRR net. A handful of sponsors have also created principal-protected, leveraged products (which couple the protection of insurance with leverage for potentially boosting returns further). I invested in another fund in this asset class (a follow-up fund to the first fund by the same sponsor), bringing my total LF holdings in litigation finance to two investments.

The sponsor has requested its identity (and all other info) be kept confidential in this article. Club members can get full info including their name, as well as detailed due-diligence, etc. here. (Membership is free but requires verifying that the applicant is truly an investor and has no conflicts of interest).

This asset class does have a J curve and takes time to deploy, mature and harvest. So it is really for longer-term money (funds that aren't needed for 7 years +).

7) Non-Real Estate Loans (versus #4 last time)

This investment is a non-real estate debt fund that has one of the most exceptional recession track records I have seen. Employees and family have almost half a billion dollars of skin in the game, and it has won many industry awards. It's also the #1 investment for members of Tiger 21 (investment club that requires $10 million in investments, minimum, and a $30,000/ year membership fee). I can say that I was impressed with the sponsor's diligence and competence during the Covid-19 crisis (and prior to that the Great Recession). I feel glad I chose to put my money with a sponsor that has been through a deep recession before. The sponsor has requested its identity and additional info to be kept confidential in this article. Club members can get full info including the sponsor's name, as well as detailed due-diligence, etc. here. (Membership is free but requires verifying that the applicant is truly an investor and has no conflicts of interest.)

8) Startups (versus #10 last time)

Most startups fail, and even the successful ones are usually white-knuckle roller-coaster rides.

When I was a serial entrepreneur, it was my job to ride that roller coaster. But now that I’m a passive investor, I don’t want that extra stress from my investments. I’d rather pay the sponsor to do all the worrying.

So when I invest in a startup, I mentally write the entire investment down to $0 in my portfolio and budget. I assume the money is gone.

If I’m not comfortable doing that, then it’s a signal that I shouldn’t be making the investment in the first place. And in those cases, I simply don’t invest. That way, if the company goes to zero — which is statistically the most likely outcome — I’m not going to lose even a second of sleep over it. And if it ends up doing well, then it’s a great bonus to celebrate… but not something I was counting on. Since last update, I had one startup successfully exit (an investment in Verivend). Details are confidential to investors-only. And the other active startup is a bank called GulfSide Bank (in Sarastota, Florida). I chose them because the CEO had an exceptionally low default rate during the Great Recession (at a previous bank). And it is doing very well and continuing to grow deposits, revenue, and profits (and defaults continue to be very low). And that's been during a tough environment for small banks. So I'm very happy with the job management has been doing.

Like most VC investments, this is not expected to produce distributions until a successful exit occurs.

9) Dislocated non-real estate loans (versus #7 last time)

As I mentioned in my previous update, I have set aside a considerable amount of cash. The idea is to be able to take advantage of dislocated and distressed opportunities caused by the next recession (and when cash becomes king). There's no guarantee there will be an opportunity to do this, or that it will be profitable. But this is how many small fortunes were built after the Great Recession.

This particular fund was designed to take advantage of dislocated, non-real estate debt. It's not a distressed fund, so they're not looking for deals that are in trouble. Instead, they're looking for healthy, cash flowing loans that can be purchased at a significant discount due to market dislocations and distressed sellers. So this takes on less risk than a distressed fund strategy.

The sponsor has an exceptional recession track record and has run multiple funds similar to this one successfully in the past. And there's no guarantee the sponsor will be able to deploy all the funds (and will just depend on what they see available).

The sponsor has requested its identity (and further details) be kept confidential in this article. Club members can get full info including their name, as well as detailed due-diligence, etc. here. (Membership is free but requires verifying that the applicant is truly an investor and has no business connections to sponsors).

10) Music Royalties: (versus #6 last time)

Music royalties have historically been very recession-resistant and not correlated with traditional and/or real estate asset classes. So this non-correlation can provide protection diversification to a portfolio during a downturn. Target returns in the industry can be high single digits to low teens net IRR. The sponsor has requested its identity (and further details) to be kept confidential in this article. Club members can get full info including their name, as well as detailed due-diligence, etc. here. (Membership is free but requires verifying that the applicant is truly an investor and has no conflicts of interest).

11) Front Street Capital (versus #10 last time)

This is my smallest holding (about 0.5% of my productive portfolio)

Front Street has over 30 years of experience, with $100 million in capital, and hasn't lost investor money across multiple cycles. They develop and acquire office, healthcare mixed-use, and industrial properties with conservative 65% LTV target leverage.

Normally, I avoid ground-up construction at the stage of the cycle this launched. However, Front Street eliminated the normally substantial refinance and interest rate risks by lining up the permanent loan in advance. And they also eliminated most or all of the tenant lease-up risk by placing the tenant in advance. So I felt comfortable making an exception for them on this.

And they started strongly but then got caught in the same office downturn that has hammered the entire industry very hard (and which started with Covid-19 and the switch to remote work).

Many office deals have gone bankrupt in this long and extended downturn. And investors in those deals have taken catastrophic realized losses.

By contrast, Front Street has not had to default or liquidate the entire fund at a distressed price. So that has been good to see.

They have paused distributions until conditions improve. I consider that a prudent decision. And all office sponsors are in a tough position and none could have predicted in advance how COVID-19 would change office demand in the way that it did. So it’s hard to blame any sponsor for something completely outside their control.

One potential silver lining is that many industry observers believe the office sector may have finally hit bottom and could be starting to recover. The data in the graph above also appears to suggest something similar. If that’s the case, it would certainly provide some welcome relief for many office investors. And we’ll see how things develop.

What's next? (My strategy for the future)

So what will I be doing next?

I've been doing a deep dive on many of the latest AI products over the last several weeks. And I believe it's hit a notable and important tipping point. In a very short time (just 6 months), I feel AI has transformed from something that was underwhelming, disappointing, frustrating and annoyingly over-hyped -- into something that is currently revolutionary and extremely likely to accelerate in the future. And if this happens, there will most-likely be significant opportunities for new investments, and also significant dangers. So, I'll be starting an article series on this shortly -- starting with my "sputnik moment" a few weeks ago when using the latest Claude Code . I'm a former senior software developer, tech project leader and IT manager. And I was flabbergasted to see Claude re-create from scratch an entire software project that took a hired programmer 1.5 months to complete and cost me thousands of dollars -- in just 5 hours and at a cost of $12.50. And it also came up with unique ideas that never occurred to (or were too much work for) the very good human programmer I'd hired... and it produced a better final design with more useful features than the original. And this is just the tip of iceberg, as software development is just the beginning of the radical changes that I believe are very likely to occur (and which I will talk about in this series).

In the meantime, what about my other alternatives?

My strategy is mostly unchanged from last time.

Invest in asset classes that are uncorrelated with the business cycle (GP stakes, litigation finance, etc.).

Invest in real estate and business cycle sensitive investments only when they're exceptional and they have high downside protection. Real estate deals must have full cycle experience, high co-investment, no floating rate debt and no unorthodox risks (i.e. no junk-rated securities, no early redemption features and everything needs to be high quality).

And my opinions and strategy will change if we get some better or worse news.

Bonus: How I Manage Cash

Here's how I manage my cash. What I do has changed over time (and is based on the current environment and rates).

In the past, I would often store cash in a bank savings account, CD or money market. But in today's environment, the yield is often quite low.

So some people like to constantly hop around and use temporary "new account" bonuses to boost that yield (and that might go for a few months before reverting lower). I generally find that continual churn and effort to be be more work than it's worth.

Others like to use broker CDs that have slightly higher rates than the banks. But these are usually callable (meaning that if the return gets high, it's probably going to get called and the investor's yield reduced). So I generally avoid these.

Right now, I'm typically using a U.S. treasury ladder.

Treasuries are backed by the full faith and credit of the US government and are currently considered to be one of the lowest risk investments in the investing universe.

And a ladder invests in treasuries with different maturity lengths (like three-month, six-month, one-year etc.).

Every 3 months or so, a rung matures and produces cash. So I look and see if I need to use it. If so... great. If not, it gets rolled into a new rung.

So it's both constantly productive while providing continual liquidity.

And currently treasuries range from about 3.6 to 4.6% (but vary over time)

I also have invested in U.S. Treasury I-bonds. They have an inflation-adjusted component, currently yielding about 4%. The biggest hitch is that there's a strict limit of $10,000 per investor per year. There are techniques to save more than the $10,000 limit with spousal accounts, children, trusts, etc. However, these still have relatively low limits and so it's not something that will work with a larger cash holding.

Some people also like to use a ladder strategy with municipal bonds (especially those who live in states with a significant income tax).

These are backed by local governments and other similar entities and so do have a slightly higher risk of default than the U.S. government.

But they are also usually tax free.

Currently the 5 year muni (municiple bond) yields 2.3185% (tax-free). So the equivalent taxable yield (at 37% federal marginal tax bracket) is 3.68%. I live in Florida, so don't have state income taxes to worry about. But if I did, then the equivalent taxable yield would be higher. So for me (in Florida), U.S. treasuries are clearly a better bang for the buck. But muni's can make better sense for others. Also, different rates are changing over time. So it's good to keep a pulse on the market.

In the past I would also sometimes use a "breakable CD" technique to juice the return a bit (and will again if those rates go up). What I would do is put the money into five-year CDs (or whatever is yielding the most) with a low penalty for breaking them. And to minimize the penalty fees, I would break up the money into a bunch of little CDs and only liquidate what I need (so I would only get penalized for that amount).

For example, if I wanted to do this with $100,000 of cash, I would break it up into five CDs of $20,000 each. Then if I needed $20,000 in cash, I would break just one of them, pay a modest couple months interest penalty on that alone, and continue to draw full interest on the others. Here's a site that highlights the penalties on different CDs.

Bonus: Investment by Investment Deep Dive on Taxes

Another thing people ask me a lot about is the tax treatment of the different items in my portfolio. This can sometimes get complicated, so many people skip thinking about it. However, doing that can lead to expensive mistakes. So I think a smart investor should always think about the after-tax return of an investment when looking at it.

At the same time, minimizing taxes isn't my first goal. Yes, I put a lot of time and thought into making sure that I minimize my tax burden as much as possible. But if forced to choose between minimizing taxes and preservation of capital/reduction of risk, I'll choose the latter every time. Someone coming from a different risk tolerance and financial situation might feel very differently.

Or to put it another way: I'm often fine with losing a few percentage points of projected after-tax return if it gives me extra diversification, safety and/or protection of principal. So you won't see me loading up 100% of my portfolio with the most tax-efficient investments possible.

My situation

I live in Tampa, Florida and am lucky in that I have no state income tax. (We do have a sales tax but it applies to purchases and not to income). I also have a relatively small percent of my portfolio in a tax-sheltered self-directed IRA and a solo 401k. So, I try to save that for investments that have much worse tax treatment than real estate.

And in general a self-directed IRA or solo 401(k) can be a good way to save on taxes. See "How to Liberate Your IRA / 401k to Invest in Real Estate" for more info.

My portfolio tax breakdown:

Residential rental properties: This is taxed at passive income rates. Due to depreciation, distributions were 35% shielded from taxes last year (which is really nice). The Tax Cuts and Jobs Act also created a 20% Qualified Business Income (QBI) deduction for many pass-through businesses, including certain rental real estate activities. This provision is currently scheduled to expire after 2025 (i.e. 2026 tax year) unless Congress extends it, so its future remains uncertain.

MG properties group: Distributions are 100% shielded from taxes. Additionally they have traditionally given their investors the option at the end of the holding period to do a 1031 exchange into a new property. This defers paying back depreciation and paying capital gains. An investor can repeat this over and over and effectively delay paying taxes forever. Even when the investor dies, their heirs inherit it on a stepped-up basis and don't have to pay the taxes either. And the results of this can be dramatic over time (and difficult to match in any other asset class):

For more on this, see "How to Invest in Passive Real Estate Without Paying a Penny of Tax (Legally): Part 2: "Defer, Defer and Die".

Front Street: Distributions are 50% shielded from taxes. Also potential for additional 20% in QBI tax shielding.

Litigation finance: I've seen different funds structured and categorized differently. A common setup is income that is considered capital gains (which can be very tax beneficial when it is long-term) and ordinary gains (which is taxed at ordinary income rates, and thus not any tax benefit).

Non-real estate business loans: Like most of the funds in this asset class, this one has no special tax benefits and is simply tax-deductible ordinary income rates.

GP Stakes: I've also seen these structured and categorized differently. One setup is capital gains on carry (which is tax beneficial) and ordinary income on management fees (which is taxed at ordinary income rates, and thus not any tax benefit).

Lessons-learned from the portfolio so far

• Diversification across strategies matters: Different alternative asset classes move through their own cycles. Holding a mix of strategies helps avoid relying too heavily on any single sector at the wrong time.

• Vintage diversification is important: The economic environment when capital is deployed has a major impact on outcomes. Spreading investments across multiple vintages helps avoid concentrating capital at the top of a cycle and increases the chances of capturing opportunities during downturns. This take planning and patience but is well worth it.

• Discipline during strong markets is valuable: During long up-cycles it can be very tempting to get too aggressive. Maintaining discipline and avoiding overly aggressive deals can improve survivability when the cycle eventually turns.

• Income helps stabilize a portfolio: Income-producing investments can provide resilience during periods when capital appreciation is temporarily weak or delayed.

• Taxes matter more than most investors realize: The difference between taxable and tax-deferred returns can dramatically change long-term outcomes, even when the raw returns appear similar.

Discussing your own portfolio and learning more

Private Investor Club members have been discussing their portfolio designs for years. And there's also been detailed discussion on thousands of sponsors and deals (including due diligence and real-life investor experiences).

If you're already a member, click here to discuss further:

If you're not yet a member, then joining is free.

To protect all members and keep the conversations useful and confidential, all applicants are required to verify that they're solely investors (and not investment sponsors, platforms or their affiliates)

Click here to learn more or to join.